In the Australian property landscape, the path to funding is no longer a straight line to the “Big Four.” For property developers and investors, the choice between non-bank vs traditional banks has become the most critical decision in the pre-construction phase.

While traditional banks have been the bedrock of finance for decades, the goalposts have shifted. Tighter regulations and a decreased appetite for “complex” risk mean that many high-quality commercial projects are being stalled at the starting line. This is where the non-bank sector has stepped up, offering a solutions-focused alternative that prioritizes project viability over rigid tick-box criteria.

At Zolve, we live and breathe this distinction. We understand that when you’re looking at land acquisition or a multi-unit development, you aren’t just looking for money—you’re looking for a partner that moves at the speed of business.

Understanding the Landscape: Traditional Banks

Traditional banks (ADIs) are highly regulated entities. Because they hold public deposits, they are governed by strict capital adequacy requirements. This often leads to:

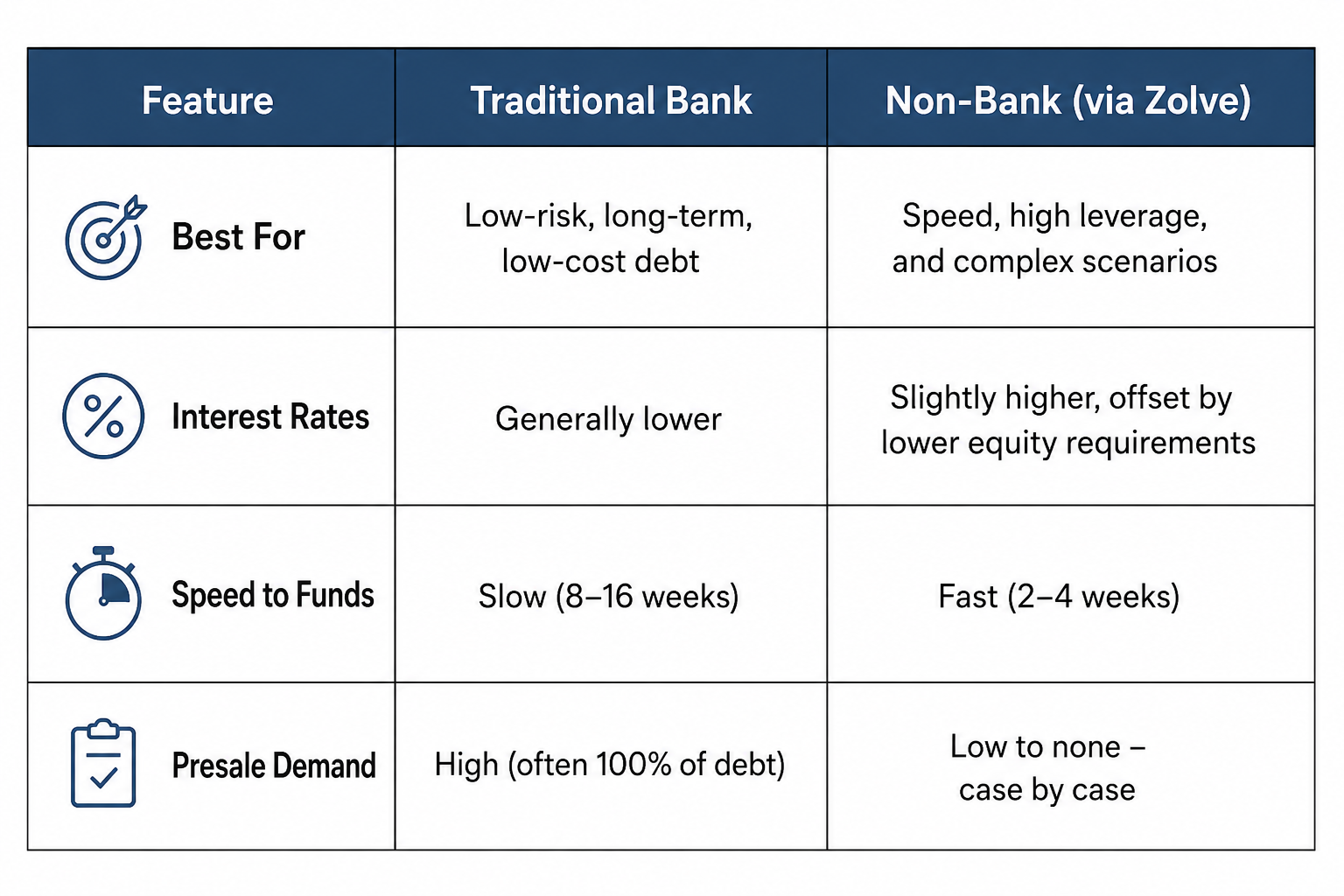

- Strict Presale Requirements: Banks often demand a high percentage of debt coverage through presales before a single brick is laid.

- Longer Approval Cycles: It isn’t uncommon for a commercial loan to take 3 to 6 months to move from application to settlement.

- Rigid Lending Criteria: If your credit history has a “blip,” or if your project doesn’t fit a standard profile, the answer is often a flat “no.”

The Non-Bank Alternative: Speed and Flexibility

Non-bank lenders don’t take deposits; they use private capital or institutional funding. This allows them to be far more agile. When comparing non-bank vs traditional banks for commercial projects, the non-bank sector wins on three fronts: Speed, Flexibility, and Complexity.

Why Developers are Choosing Non-Banks:

- Lower Presale Hurdles: Many non-banks offer “stretches” on leverage or allow for lower presale targets, letting you start construction sooner.

- Tailored Terms: Instead of a “one-size-fits-all” product, non-banks can structure interest capitalisation and fees to suit your project’s cash flow.

- Fast Execution: At Zolve, we’ve seen non-bank lenders issue indicative terms in 48 hours and settle in a fraction of the time a traditional bank would take.

Zolve: Your Bridge to Private Capital

Deciding between a non-bank vs traditional bank isn’t always about who is “better”—it’s about what is best for this specific project at this specific time.

At Zolve, we act as your expert guide. We aren’t a lender ourselves; we are a commercial broker with a massive network of independent non-bank and private lenders.

What makes Zolve different?

- Full-Service Guidance: We don’t just give you a list of names. Our Loan Specialists manage the process from the first conversation to settlement.

- The “Tricky” Specialists: If your scenario is complex—perhaps involving land banks with no immediate income or a developer with a non-traditional credit profile—we know exactly which lender has the appetite for it.

- Independence: Our lenders are independent. This means we focus entirely on finding the right fit for your needs, not a bank’s bottom line.

Why Choose Zolve

Learn More

Case Study: Unlocking Top Loan Terms—In Only 24 Hours

The Scenario: An experienced developer in Melbourne recently approached Zolve for a construction facility for a townhouse site. They had their bank broker working on a construction facility via a major bank.

The Zolve Solution: Zolve obtained competitive terms within 24-hours via a non-bank lender, who specialises in townhouse developments, offering greater funds at settlement, flexible terms, rates close to bank rates and the ability to settle in 3-4 weeks.

The Result:

- Loan Amount: $3.2M construction facility.

- LVR: 70% net on land and 75% on NRV (finished value)

- Timeline: Terms issued in 24 hours

Finding the Right Fit

In the debate of non-bank vs traditional banks, the “best” option depends on your equity position, your timeline, and your project’s complexity. If you have plenty of time and a “perfect” application, a bank might work. But if you need to seize an opportunity, minimise presale pressure, or solve a complex funding puzzle, the non-bank sector is often the superior choice.

At Zolve, we make the “hassle-free” promise a reality. We take the stress out of the search so you can focus on what you do best: building the future.

Get Your Commercial Funding Checklist

Navigating the world of commercial finance can be daunting. We’ve put together a “Commercial Project Funding Readiness Checklist” to help you gather exactly what you need to impress a lender and secure a “Yes.”

Commercial Project Funding Readiness Checklist:

This checklist is designed to help you prepare your commercial loan application and increase your chances of securing the funding you need.

Company & Borrower Information:

- Company Registration: Ensure your company is properly registered and in good standing.

- Borrower Profile: Prepare a detailed summary of your business, its history, and its key personnel.

- Credit History: Check your business and personal credit scores. Address any issues beforehand.

Project Details:

- Project Description: Create a comprehensive overview of your project, including its scope, timeline, and objectives.

- Market Analysis: Provide research on the market demand for your project, including competitor analysis and pricing strategy.

- Feasibility Study: Include a detailed feasibility study that assesses the technical and financial viability of your project.

Financial Information:

- Financial Statements: Prepare up-to-date financial statements for your company, including balance sheets, income statements, and cash flow statements.

- Project Budget: Develop a detailed project budget that covers all costs, including construction, permits, marketing, and contingencies.

- Cash Flow Projections: Provide realistic cash flow projections that show how you plan to manage project finances and repay the loan.

Collateral & Guarantees:

- Collateral Valuation: Have all collateral valued by a qualified appraiser.

- Guarantees: Be prepared to provide personal guarantees or other forms of security.

Legal & Regulatory Compliance:

- Permits & Approvals: Ensure you have obtained all necessary permits and approvals for your project.

- Environmental Assessments: Conduct any required environmental assessments.

Required Documentation:

- Loan Application Form: Complete the lender’s specific loan application form.

- Supporting Documentation: Gather all supporting documentation, such as financial statements, project plans, and legal agreements.

Professional Support:

- Commercial Broker: Consider working with a commercial broker to help you navigate the lending landscape and secure the best loan terms.

- Accountant: Consult with an accountant to ensure your financial statements are accurate and complete.

- Lawyer: Engage a lawyer to review all loan documents and ensure legal compliance.

This checklist is intended as a general guide only. For tailored funding advice, speak with a Zolve Loan Specialist

Zolve – The Funding Specialists

Ready to see what the non-bank sector can do for your project?

Contact a Zolve Loan Specialist today and let’s get your project moving.